Depreciation

Definition

Depreciation is the systematic allocation of the cost of a tangible fixed asset over its useful life. It reflects the wear and tear, obsolescence, or usage of an asset as it contributes to revenue generation.

In accounting, depreciation is a non-cash expense that reduces the book value of an asset and appears on the income statement as an operating expense.

Origins

The concept of depreciation emerged in the 19th century as industrialization led to widespread use of machinery. Businesses needed to account for asset aging and capital maintenance. Today, depreciation is a core principle in GAAP (ASC 360) and IFRS (IAS 16), essential for matching expenses with revenues.

Usage

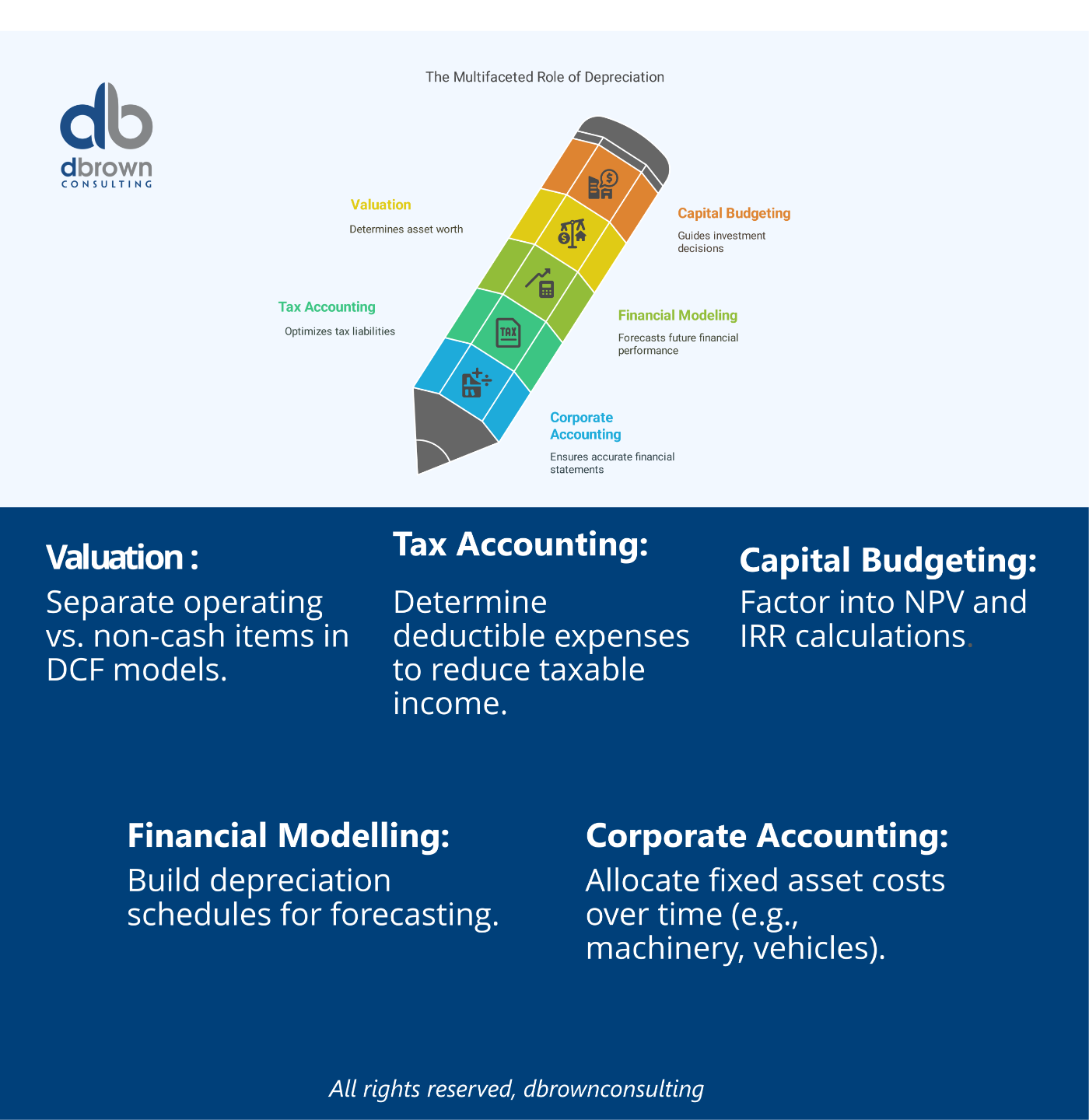

Industry Applications:

-

Corporate Accounting – Allocate fixed asset costs over time (e.g., machinery, vehicles).

-

Tax Accounting – Determine deductible expenses to reduce taxable income.

-

Financial Modeling – Build depreciation schedules for forecasting.

-

Valuation – Separate operating vs. non-cash items in DCF models.

-

Capital Budgeting – Factor into NPV and IRR calculations.

How Depreciation Works

When a company buys a tangible long-term asset, it doesn’t expense it immediately. Instead:

The asset is capitalized on the balance sheet.

Depreciation is recorded each period to allocate its cost over useful life.

This reduces both:

-

Net income (via depreciation expense)

-

Net book value (via accumulated depreciation)

Depreciation does not affect cash flow directly, but it reduces taxable income, thereby saving taxes (a tax shield).

Key Takeaways

- Depreciation reflects asset consumption over time.

- It spreads CapEx over periods that benefit from the asset.

- Provides a tax benefit due to reduced taxable income.

- Affects key metrics like EBIT, but not EBITDA (non-cash).

- Different methods impact the timing and amount of depreciation.

Types & Variations of Depreciation

Method |

Description |

|---|---|

|

Straight-Line (SL) |

Equal depreciation each year. |

| Declining Balance (DB) | Accelerated method—more depreciation in early years. |

| Double Declining Balance (DDB) | 2× straight-line rate on declining book value. |

| Sum-of-the-Years'-Digits (SYD) | Accelerated method based on digit weighting. |

| Units of Production (UOP) | Based on usage/output rather than time. |

| MACRS (Tax) | IRS-mandated method in the U.S. for tax reporting. |

Context in Financial Modeling

Depreciation plays a major role in:

- 3-statement modeling:

Reduces EBIT

Affects taxes

Added back in operating cash flow

-

CapEx modeling: Depreciation is forecasted based on past CapEx trends.

-

DCF Valuation:

Impacts FCFF / FCFE

Drives net working capital and reinvestment assumptions

- Fixed Asset Schedules:

Model asset roll-forwards: additions, disposals, accumulated depreciation

Nuances & Complexities

-

Book vs. Tax Depreciation:

-

Book: Used for financial statements (GAAP/IFRS).

-

Tax: Often accelerated for tax savings (e.g., MACRS in U.S.).

-

-

Useful Life Estimation:

-

Subjective, impacts depreciation expense.

-

-

Salvage Value:

-

Residual value estimated at end of asset life.

-

-

Asset Impairments:

-

If value drops significantly, depreciation may no longer apply—impairment is recorded instead.

-

Mathematical Formulas

1. Straight-Line Depreciation:

2. Declining Balance (Double Declining Example):

3. Units of Production:

4. Accumulated Depreciation:

Master Financial Modeling with the FMA

Change your career today by earning a Globally Recognized Accreditation

Develop real-world financial modeling skills, gain industry-recognized expertise, stand out and start earning more by gaining the Advanced Financial Modeler (AFM) designation from the Financial Modeling Institute.

Our expert-led online cohort based program covers everything you need to become a world class financial modeling pro and advance your career in finance.

Related Terms

-

Capital Expenditures (CapEx)

-

Amortization

-

Asset Impairment

-

EBITDA

-

Accumulated Depreciation

-

Net Book Value

-

MACRS / Section 179 (U.S. tax code)

Real-World Applications

1. Tax Planning

A company accelerates depreciation using MACRS to lower taxable income and increase cash flow in early years.

2. Investment Analysis

An analyst adjusts EBITDA by stripping out depreciation to compare operational performance across companies.

3. CapEx Modeling

A logistics firm builds a 5-year depreciation schedule for $25M in trucks, assuming a 7-year useful life and 10% salvage value.

4. M&A Due Diligence

Buyers analyze historical CapEx and depreciation policies to evaluate maintenance vs. growth CapEx needs post-acquisition.

References & Sources

Unlock the Language of Finance!

Elevate your financial acumen with DBrown Consulting’s exclusive newsletter. We break down complex finance terms into clear, actionable insights—empowering you to make smarter decisions in today’s markets.

Subscribe Today & Make Financial Jargon Simple!

We won't send spam. Unsubscribe at any time.